Skip to content

Skip to content

Form 1040 Schedule A

Some tax filers have expenses that are deducted from their gross income to help them pay lower taxes. If the deductions are higher than the standard deduction, these individuals can itemize their deductions using a Form 1040 Schedule A.

Schedule A has seven categories for expenses, which include medical expenses, donations, and even mortgage interest. However, there are strict rules when calculating and claiming deductions, and in some cases, you might not want to deduct the full amounts.

The good news is you don’t have to complete every line of this form. For example, if you don’t have expenses in a category, you can skip them. Once you’ve finished, you’ll add up your total deductions and add them to Form 1040.

It’s important to note if you have over $1,500 in taxable interest from investments, you may have to fill out a Schedule B.

Schedule C

Schedule C is part of Form 1040. Self-employed individuals need to fill out a schedule C to report their gross profit or loss. They can also choose to fill out a list of itemized deductions or take the standard deduction.

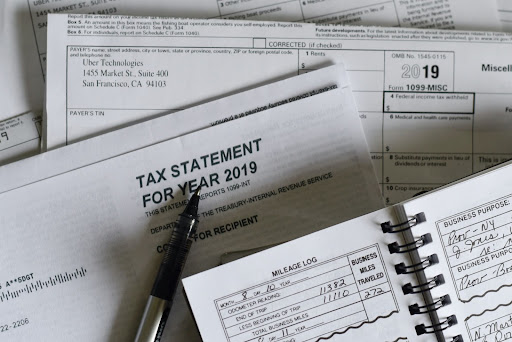

Form 1099-INT

Form 1099-INT is for interest income. You would receive this information from banks and other financial institutions if they paid you interest on deposits. Any interest you make is taxable and will need to be listed on your tax return.

All of the interest earned that’s reported on the Form 1099-INT will be added to your return. You should also fill out a Schedule B with the names of the payers and the amount of interest earned.

Form 1099-MISC

Form 1099-MISC is also for self-employed individuals. They should receive this form from their clients at the end of the year, reporting the total amount received. Any income reported on a 1099-MISC should be reported on a tax return.

For freelancers, contractors, and other self-employed individuals, Form 1099-MISC replaces the W-2 you’d receive from your employer. Landlords may also be required to file a 1099 MISC for payments made to employees, attorneys, and contractors.

Being self-employed means more complicated taxes than those with employers, so consider investing in tax software that can help you calculate your quarterly and annual taxes.

Form W-4

When you first started your job, you probably filled out a W-4. This form isn’t filed with your tax return or sent to the IRS; instead, it’s used to help your employer figure out how much to withhold from your paycheck for taxes. If you change employers, you’ll need to file a new W-4 with your new employer. You should also fill out a new W-4 if you have any life changes, such as having a child, as you’ll need to claim a dependent.

Form W-2

Form W-2 is another common tax form that many people already know about. Unfortunately, Forms W-4 and W-2 are often confused with one another. While your employer holds on to your W-4 so they can accurately take taxes out of your paycheck, your W-2 is given to you by your employer. You’ll receive this form at the end of every year to show the total amount of taxes that were taken out of your paychecks.

Your employer will also send a copy of your W-2 to the IRS and other tax authorities. The good news is because your employer already sends this to the IRS, you won’t need to file it with your tax return if you lose it. However, you should keep your W-2 on hand so you know your gross and net incomes and can accurately calculate your taxes.

Form 8949

Form 8949 is used to report capital assets, including stocks, bonds, and cryptocurrency. Remember, you’ll need to report any money earned throughout the year, even if you didn’t earn it through regular work. On Form 8949, you’ll report your gains and losses while providing information about your investments assets. This information includes:

- Description of assets sold

- Date asset was acquired

- Date asset was sold

- Proceeds from the sale of the asset

- Gains and losses

Final Thoughts

Not everyone fills out the same tax forms. You must learn about which forms you’ll need to fill out based on your employment situation, investments, and overall financial situation. Remember, these are just a few of the most common forms. If you sell products, you’ll also need to learn about other types of business tax forms to cover sales tax and payroll tax. You can explore the top payroll companies here.

If you’re not sure which forms you should fill out come tax season, consider working with a qualified accountant. Knowing which forms you should fill out can help you save time during tax season; instead of panicking trying to figure out what you need to do to file your taxes, you’ll already have the correct forms in hand and can begin working on them at the end of the year.

If you’re a small business owner or self-employed individual, make sure you’re tracking your income and expenses throughout the year so you can accurately pay your taxes and won’t have to worry about paying any fees.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}